WELCOME TO THE VN CAPITAL PARTNERS ONLINE EXPERIENCE

This portal is for investors, qualifying potential investors, and IFA’s alike.

Information about our company, the team, and SPV projects can all be found here, together with individual project videos.

The purpose of this site is threefold:

- To provide qualifying potential investors sufficient information about VN sponsored projects to allow them to make an informed investment decision

- To provide existing investors visibility of their current VN project portfolio and update information on the particular SPV’s they have invested in

- To provide VN-CP registered IFA’s, Wealth Managers and Intermediaries the following support;

- Project and due diligence information for compliance

- Individual support and bespoke services to enable clear and concise advice to clients

- Introductory fee structures and incentives.

But before you enter the site let me draw your attention to what should be obvious but because of marketing language such as low or medium risk’ used by certain promoters and product providers, may not be. All SEIS and EIS Projects are a gamble or in racing vernacular a ‘Punt’ and VN sponsored projects particularly so, as they deal with ‘bleeding edge and disruptive technology developments’.

This should not alarm you however, just alert you the first rule of investing i.e. ‘Use Common Sense’.

Please read on and enjoy the site content, we seek to constantly improve our communication with visitors so all feedback (good & bad) is appreciated.

Thank you for the interest in our company and our sponsored projects.

Kind regards

David Newman

Chairman

To be successful at any form of gambling you need to fully understand the opportunity, risks, odds, marketplace and competition. If these factors are not considered, then the likelihood of losing all your money is extremely high. SEIS and EIS are by definition ‘High Risk’ – ‘High Reward’ opportunities, where if the same processes are not followed the outcome is almost certainly to be the same as a ‘Bad day at the racecourse’.

If we accept this assumption, then what exactly is the difference between investing in Tax Incentivised Alternative Investments and a ‘Punt’ on the Grand National?

Simply put, a bookmaker will take all money placed with him and give ‘risk vs reward’ odds on a specific gamble. If the gamble fails, you lose all money placed, in other words a ‘no stop loss’ proposition. If the gamble is successful, you are rewarded at the odds agreed and pay no tax on the winnings.

With an SEIS Investment (maximum £100k per individual pa) the Exchequer allows 50% of all monies invested to be immediately set off against income tax due, and in the event that the project fails, a further 45% of of the balance can be claimed as loss relief. So the actual gamble has a ‘stop loss’ position of 27.5p in the pound.

In the event of a successful project, subject to the shares being retained for the minimum 3-year period, all gains made are free from tax (CGT or Capital Gains Tax).

With an EIS Investment, (maximum £1m per individual pa) the Exchequer allows 30% of all monies invested to be immediately set off against income tax due, and in the event that the project fails, a further 45% of of the balance can be claimed as loss relief. So the actual gamble has a ‘stop loss’ position of 38.5p in the pound.

In the event of a successful project, subject to the shares being retained for the minimum 3-year period, all gains made are free of tax (CGT or Capital Gains Tax).

Certain product providers and Advisors would have you believe that some SEIS and EIS projects can be a ‘Safe Bet’, a term in direct contradiction with HMRC guidelines for such investment opportunities.

Over the past 10 years or so Product Providers & Funds have been consistently marketing and selling “safe” Enterprise Investment Schemes. Some were tied into the UK Government Feed-In-Tariff strategy i.e. providing investors with ‘upfront’ tax relief and ‘guaranteed ‘exit profits’ via renewable energy development schemes. This practice was fortunately outlawed by Government in the last budget, but not before it had cost UK SME’s hundreds of millions of pounds in lost investment. Is that the end of the story, well if we look at HMRC’s approach taken in hindsight toward Film Schemes, one might argue that the possibility of relief withdrawal for those renewable investors is quite possible, certainly reducing the value of their ‘safe punt’ or even negating it completely.

Today those same Funds and Providers are looking for new ways to get round the rules and it is the nature of such organisations to do so as they seek a commercial edge, but for you the investor it really begs the question: ‘Why are you investing’?

Investment in an SEIS or EIS project has two completely different risk components:

1/ Income Tax / Loss Relief

2/ Project success or failure

When considering investing it is imperative to ascertain that the project has HMRC Advanced Assurance and will continue to qualify for relief throughout the life of your investment. Without this component you are simply back at the racetrack.

Risk Considerations – Is the EIS/SEIS Tax Relief at Risk?

When looking at Investments into EIS or SEIS, you should look at the nature of the company as well as the company itself, i.e. What is the business doing, and how is it doing it?

Recent HMRC clamp-downs and court cases have demonstrated that previously acceptable EIS operations are now, no longer allowed by HMRC. This area should be of particular concern to Investors, as Investments described as “Low-Risk”, “Guaranteed returns” or even “Tax free returns of X% per annum” need to be looked at very carefully indeed. If nothing else, an investor should factor in the risk of not just business success or failure, but also whether the initial tax relief will stand up to HMRC scrutiny in the future.

History has shown us that in the eyes of Government – ‘Everything is Guaranteed Until it Isn’t’. So whether you decide to invest in a “high-risk” or “low-risk” EIS or SEIS, try to remember, if it looks to good to be true, it probably is!

Project success or failure should be the only ‘risk’ component if the scheme is used correctly, and as mentioned before, some research, in-depth reading coupled with common sense Q&As, should give you enough information to make a reasonable decision, it is a Punt after all.

Some obvious questions for a start-up or development project should include, questions like:

How much does it cost to raise the funding?

Where do the fees go and for what?

What will the funding be spent on?

Is there a business plan?

What is the monthly salary bill?

What are the the operating costs?

Who are the competition?

What will differentiate this company from the competition?

Why?

For how long?

What is the projected time to market for revenue creation?

What is the projected time to market for ‘breakeven’?

What is the projected time to market for profitability?

What are the projected returns to investors?

What is in it for the Investor? How? Why?

As well as the above, the business plan should also show the timeline and deliverables and all of this should be considered by Investors to be the minimum requirements for you to spend your time investigating further.

Just like the Grand National, the excitement is palpable as you research the investment opportunities on offer deciding which project to pick. However, unlike the National you have a fixed stop-loss, which means that your maximum loss on a £1 EIS investment is 38.5p.

It is now universally accepted that once you have found the right asset allocation and picked the right investment portfolio for your needs, you still need to pick the investment products to fill it out and manage it throughout the year. As part of a strategy for a balanced investment portfolio for a High Net Worth Individual, Sophisticated Investor or Professional Investor, the high risk elements of this strategy can be equally important as the ‘low-risk’ elements when considering the overall returns of the portfolio. In fact, given recent events in the global financial markets, no asset or portfolio allocation can be regarded as guaranteed, and so all of it is effectively a gamble of sorts

However, not losing money, is also not making any money, which in investment terms is not beneficial to a portfolio when things like fees are taken into account. For example, research by JP Morgan recently found that a very basic portfolio split half-and-half between shares and bonds and held for five years would have protected investors from all but the smallest losses in recent decades.

The bank looked at all five-year periods, starting at monthly intervals, since 1950 and found that the biggest loss was 1% a year, or a little more than 5% in total.

By contrast, anyone who invested entirely in shares would have seen a maximum annual loss of 7% over five years – a much more significant combined loss of 42% after compounding.

Anyone holding this simple mixed portfolio for 10 years would never have lost money since 1950, the research found, no matter which month they started in – even if it was just before a big stock market crash.

This is not to say that a portfolio consisting of 50% shares and 50% bonds is the right one in all circumstances or for all investors. But it does illustrate the importance of considering the mix of investments in your pensions, Isa’s or other long-term savings plan.

Also when looking at a portfolio ‘risk vs reward’ needs to be considered. As a broad rule of thumb most fund managers accept that in a medium to large portfolio the numbers usually look something like this:

50% of the portfolio in capital preservation

25% in low risk growth asset backed instruments

20% in medium risk growth instruments,and

5% into high return opportunities.

The 5% element (subject to the portfolio size) should then be looked at as a whole and sub divided into investable amounts with varying levels of risk vs reward opportunities, such as SEIS and EIS.

The information provided above is in reality a ‘snapshot’ of the SEIS/EIS market opportunity and we have tried to cover the known points, as well as uncover the less well known aspects of these type of schemes.

The most important point to take from this information is simply this:

SEIS and EIS are essential tools in the Governments armoury to ‘Build a Better Britain’ within the innovation and technology development sectors. The tax breaks going in are good, and upon successful exit even better, but the projects have to be real.

![]()

David Newman

Chairman

In 2021 approximately £100 million was wagered the Grand National (Down from £200m in 2016 – Covid et al) & most of it was lost.

According to HMRC figures, approximately £1.9 billion was projected to be wagered on SEIS and EIS Alternative Investments the same year.

Since the Enterprise Investment Scheme (EIS) was launched in 1993-94, 31,365 companies have received investment and £22 billion of funds have been raised.• In 2018-19, 3,905 companies raised a total of £1,824 million of funds under the EIS scheme. This is a decrease from 2017-18, when 4,080 companies raised £2,001 million.

• In 2018-19, a total of £504 million of investment was raised by the 1,470 companies raising funds under the EIS scheme for the first time.

• In 2018-19, companies from the Information and Communication sector accounted for £543 million of investment (30% of all EIS investment).

• London and the South East accounted for the largest proportion of investment with companies registered in these regions receiving £1,193 million (65% of all EIS investment) in 2018-19.

Following the changes made regarding investment in renewable technologies and the exclusion of ‘feed-in-tariff’ from the equation, the landscape post 2016/17 looks completely different as do the projected returns.

Returns offered range from ‘get your money back’ (Octopus EIS Tranche 19) right through to projects such as VN Automotive providing 1st Round investors with gains of 25 times and 2nd Round investors with gains of 6 times.

Latest News

The FPS Waal, a vessel operated by Future Proof Shipping (FPS) has completed its last inland voyage using a diesel engine, and will now be retrofitted with a system to enable it to run on hydrogen. The retrofit is scheduled to begin this week and will be carried out by the Holland Shipyards Group shipyard in Werkendam, the Netherlands.

Much like a previously converted vessel – the FPS Maas but now called H2 Barge 1 – the FPS Waal will have its internal combustion engines completely removed before a new zero emission propulsion system is fitted. This will consist of PEM fuel cells, hydrogen storage, battery packs and an electric drive train. Holland Shipyards Group previously selected marine battery manufacturer AYK Energy to supply the lithium batteries for the retrofit.

A third container vessel retrofit is planned, one that will also be equipped with a zero emission hydrogen propulsion system – called the FPS Rijn.

The latest project is supported by grant funding from the Interreg North Sea Region Programme (Zero Emission Ports North Sea – ZEM Ports NS), Netherlands Enterprise Agency (RVO), Port of Rotterdam and Expertise- en InnovatieCentrum Binnenvaart.

Rolls-Royce has outlined plans to produce green hydrogen at its Friedrichshafen headquarters and conduct testing of its mtu hydrogen engines and fuel cell systems.

The company has also successfully completed testing of a 250 kW fuel cell demonstrator, proving its capability to provide uninterrupted power during blackout situations.

As part of the Rolls-Royce ‘H2Infrastructure’ funding project, the company aims to develop its own standardized mtu electrolysers with a capacity of up to 4 MW, scalable to over 100 MW, following its acquisition of a stake in electrolysis stack developer Hoeller Electrolyser in the previous year.

The project will involve the production of green hydrogen through PEM electrolysis, with plans to expand hydrogen production capacity to 10 MW to support the development of propulsion technology.

Rolls-Royce envisions covering a significant portion of the hydrogen value chain, including infrastructure, production, distribution, and utilization, in collaboration with Hoeller Electrolyser, with the ultimate goal of producing low-cost, large-scale green hydrogen using renewable energy sources.

Lord Bamford says internal combustion engine has a future following climbdown by Brussels

Britain must rethink its net zero ban on new petrol and diesel cars after Brussels watered down restrictions across Europe, the chairman of JCB has said.

Lord Bamford insisted that “the internal combustion engine certainly has a future”, in comments that will add to pressure for Rishi Sunak to drop a 2030 crackdown on non-electric vehicles.

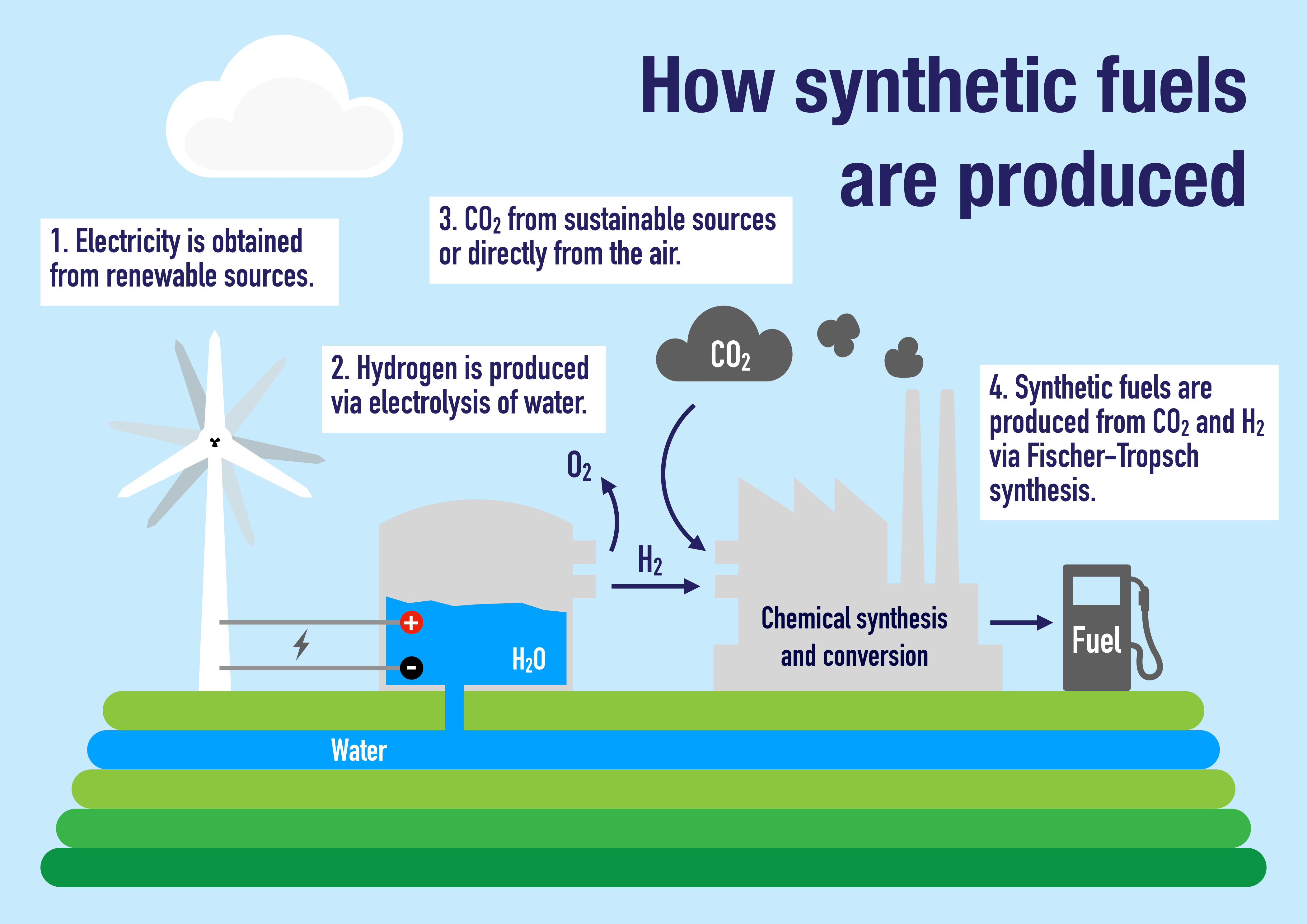

It comes after Brussels last week agreed to water down its zero-emissions vehicles mandate by allowing the sale of internal combustion engines as long as they burn carbon-neutral petrol alternatives known as e-fuels.

The move prompted some in Whitehall to consider exploring e-fuel exemption, although the Prime Minister and Grant Shapps, the Energy Secretary, stood by their existing plans when unveiling further green measures last Thursday.

JCB is already working on hydrogen-powered diggers to replace its traditional models. The business sold 75,000 machines in 2020.

Lord Bamford, a major Tory donor and one of the country's most successful businessmen, said: “The internal combustion engine has a role to play in a zero-carbon future.

“Governments around the world need to be technology-neutral, as they legislate for how best to reach net zero targets.

“Fossil fuels are the problem, not the engine itself. JCB has engineered and developed new engines that run on hydrogen gas, a zero CO2 fuel – they provide the same power and performance in our machines as their diesel counterparts.”

Britain is to ban all new non-hybrid petrol and diesel cars in 2030. Hybrids will then be outlawed in 2035, with new vehicles only permitted if they are pure electric or run on another zero-emission fuel such as hydrogen.

Petrol and diesel cars will also be banned on the Continent from 2035. But following an intensive lobbying effort by German carmakers, a carve-out was agreed that allows the sale of vehicles that can run on e-fuels – which will be made from carbon sucked out of the air and hydrogen produced using renewable energy, and so will not emit new CO2.

Lord Bamford said: “If e-fuels can be made to work in a carbon neutral way in cars, the internal combustion engine certainly has a future. Governments should be wary of outlawing engines, when the root cause of the problem is the fossil fuels we currently put in the fuel tank.

“Let’s be more open-minded about the possibilities; battery-electric technology is not the only possible solution to the problem.”

E-fuels could also offer a lifeline to smaller, specialist UK racing car makers.

Morgan and Lister, which make racing cars, are considering adopting the fuels alongside Aston Martin and McLaren.

Lawrence Whittaker, chief executive of Lister, said smaller firms risk being overwhelmed by the cost of developing combustion engines and electric drivetrains in tandem, since most markets will not ban petrol cars for many years.

India, for example, will not phase combustion engines out until 2040, meaning there will be a time when car companies will need to be making both electrics and combustion cars to cater for the global market.

Mr Whittaker said: “I don’t think the government even considers how car manufacturers are having to build dual fuel cars and what impact this is having on profitability.

“I 100pc agree that the UK should allow the sale of vehicles that use synthetic or carbon neutral e-fuels.”

The Morgan Motor Company, designer of the Plus Four roadster sports car, is also considering the benefits of the fuel if its engine supplier BMW is onside.

Toby Blythe, of Morgan, said: “If a viable e-fuel powertrain became available, via our long-term supplier, that would suit our product we would certainly consider it.”

The company is controlled by Investindustrial, the Italian investment company that previously owned Aston Martin.

Safer Aircraft Cabin Air Now A Possibility For Passengers & Air Crew Alike

LONDON, UK, March 15, 2023/EINPresswire.com/ --

Cabin Air Sensor Solutions Ltd, (CASS) announced today that they had successfully completed their 9-month compound sensing work package adding Ethanol, Ammonia, Acetone, Toluene, Tricresyl Phosphate & Carbon Monoxide to their compound detection capability.

Operations Director Mark Gilmore said, "In May 2022 the UK's National Physical Laboratory, verified the sensor’s ability to detect Tributyl Phosphate in real-time which was key in our development of the sensing technology pathway. Using the lessons learned whilst working on the TBP coating has enabled us to rapidly open a huge opportunity for the company by increasing our sensing capability to cover 5 further compounds, and a gas".

CASS also announced that their Japanese Patent Application had been granted, and that further grants are pending final investigations.

David Newman, CASS CEO said, "It has been an extremely difficult journey for a small start-up company to take this completely original Idea from Concept, though to Prototype and then, to Portable Handheld Sensor, but with the support of our private & corporate investors, together with our scientific team, we have finally made it, and are incredibly proud of the achievement".

The world’s First Real-Time, Poisonous Compound Sensor for Aircraft Cabins has been verified by UK’s National Physical Laboratory.

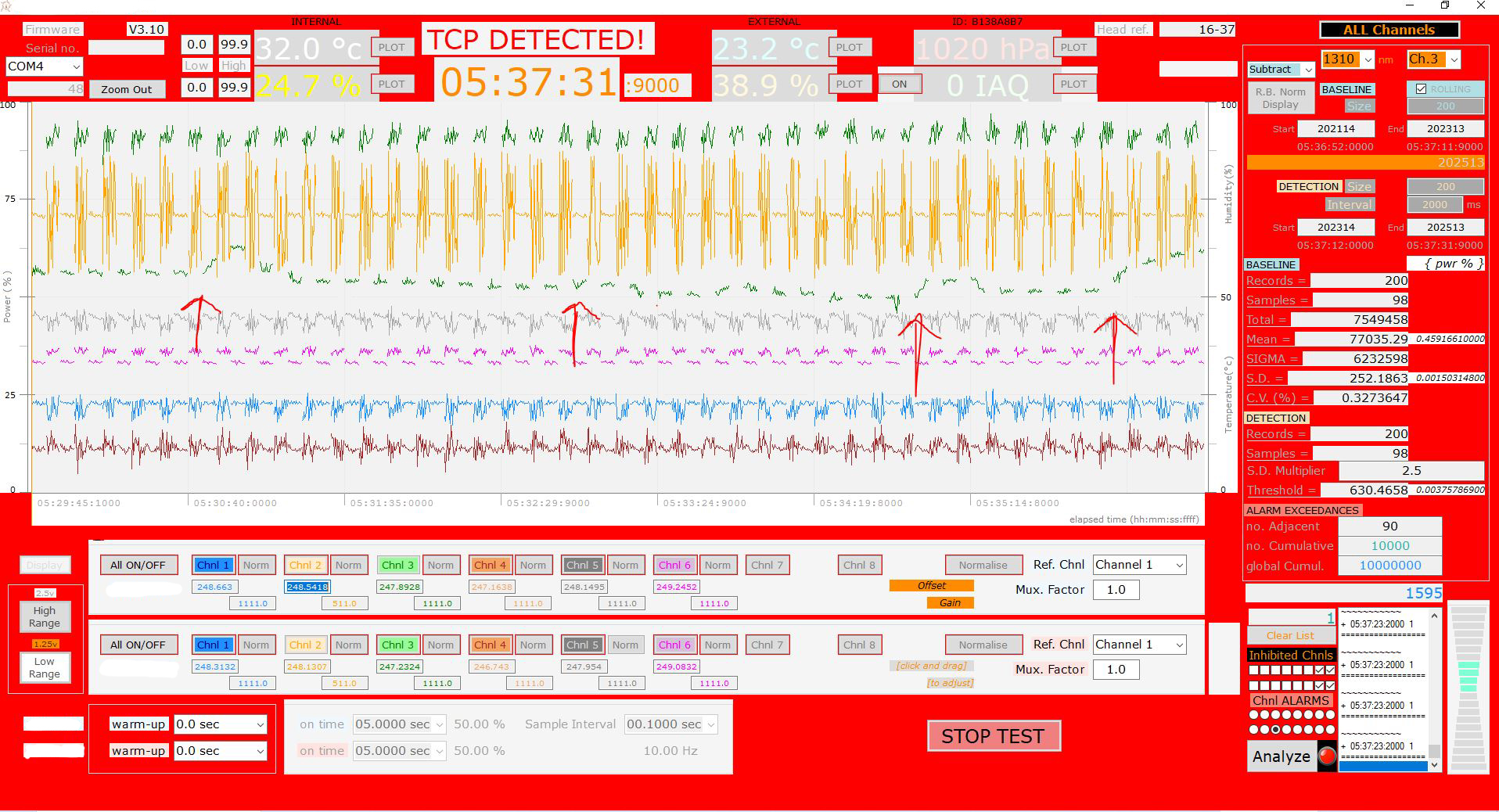

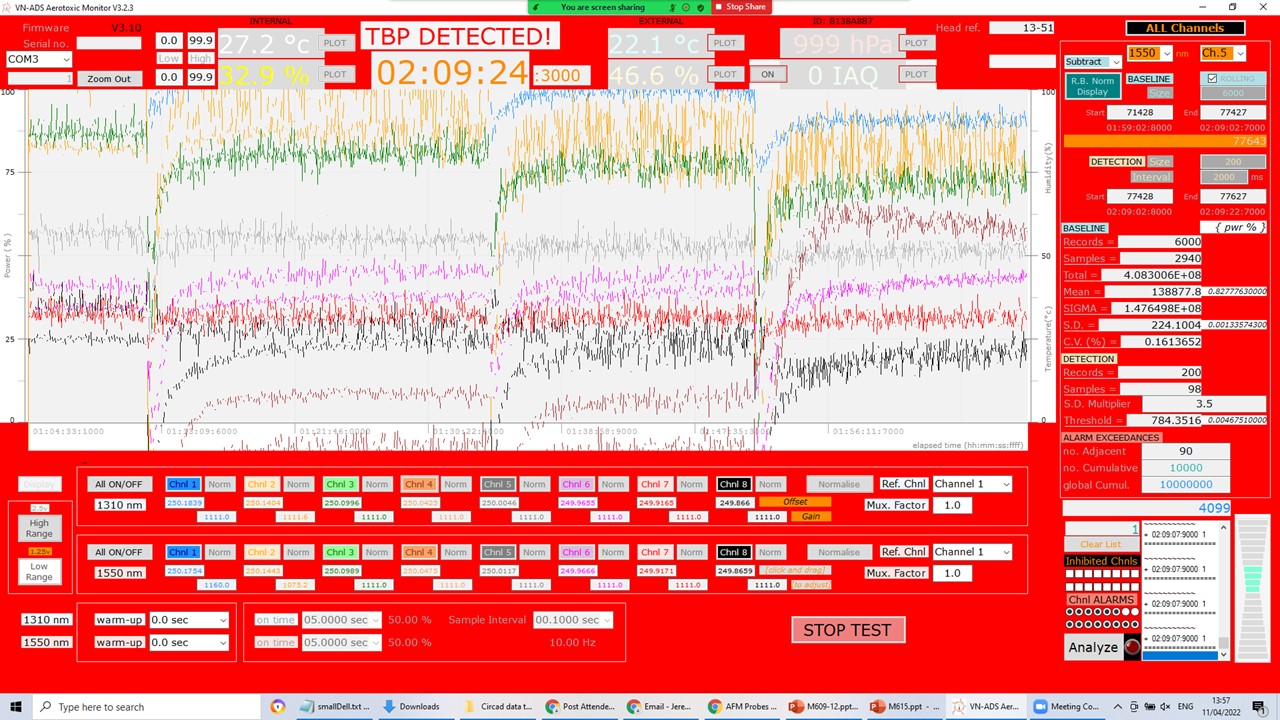

Following multiple successful in-house tests and the real-time detection of TBP, witnessed by Dr. Nicholas Martin of the National Physical Laboratory (NPL), VN Aerotoxic Detection Solutions Ltd (VN-ADS) announced today that it has successfully developed a real-time, poisonous compound sensor for use in aircraft cockpits and cabins.

For the past 5-years, VN-ADS has worked with NPL to ensure that their proprietary technology is independently validated and verified for its capabilities in selectively detecting individual Volatile, and Semi-Volatile, Organic Compounds such as Tributyl Phosphate, TBP, Tricresyl Phosphate, TCP and Triphenyl Phosphate, TPP.

VN ADS is now developing the sensor to detect other poisonous compounds found when engine seals fail, causing jet lubrication oil to be burned and toxic fumes to enter the aircraft cabin via the bleed-air / air-conditioning system.

NPL will once again deliver independent verification of the sensor’s capabilities. The sensors will then be tested in aircraft cockpits and cabins on live flights, prior to offering commercial poisonous compound sensor services to airlines, operators, and manufacturers in the aerospace industry.

Using the sensor on every flight will allow Pilots and cabin crew to know immediately ‘if and when’ poisonous compounds are present in the aircraft cabin air. They can then take appropriate action for the health and safety of themselves and their passengers, knowing that they have irrefutable evidence of a ‘Fume event’ taking place.

Whilst the health & safety benefits of using the sensor on every flight going forward are obvious for pilots, cabin crew and passengers, the ability to now sense poisonous compounds in real-time during flights, will undoubtably become an influencing factor when Judges decide the merits of the ever-growing number of legal actions initiated by pilots, cabin crew & their unions, claiming long-term health issues caused by Aerotoxic ‘Fume Events’.

VN-ADS CEO David Newman said:

“Despite Clean Air legislation being passed by the US Senate 2-years ago, and an investigative program set up by the Federal Aviation Authority, until this announcement no ‘Real-Time’ poisonous compound sensors exist. As such for the past 50-years, the Aviation industry has been able to ignore / deny the growing problem of ‘Fume Event’ based aircrew health problems. That position changes today”.

- Bloomberg NEF estimates that there will be an $11 trillion investment in production and storage of hydrogen worldwide through to 2050.

- In 2020 Europe announced its path to 100% renewable hydrogen by 2050.

- EU estimates that clean hydrogen could supply 24% of the world’s energy demand, with annual sales of approx. €630 billion.

- EU’s objective to support installation of 6G of renewable hydrogen electrolysers to produce approx. 1m tonnes of renewable hydrogen.

- EU also states hydrogen to become intrinsic to Europe’s integrated energy system by 2030. At least 40 gigawatts of renewable hydrogen electrolysers to produce approx. 10m tonnes of renewable hydrogen by 2030.

- Large corporates now shifting focus to transition to hydrogen as part of their energy strategy, e.g. Cummins Inc, BP, BG, Navistar Inc, Shell, Air Liquide/Air Products, Linde etc.

Over the last 8 years the team at HPGS has worked on delivering the most flexible, efficient and easily manufactured hydrogen technology available by developing an electrolyser solution that integrates the recovery of waste energy to deliver green hydrogen solutions.

The ability of the HPGS solution to recover both heat and motive power from waste energy in existing power generation plants delivers 'real' green hydrogen, expanding both the boundaries and real commercial/industrial opportunities for generator owners and operators alike.

HPGS is projecting that its solutions will cost 50% less that conventional PEM solutions and be 25% more efficient, manufactured with off-the-shelf components and inexpensive materials.

Immediate Opportunity

Using existing sample collection methods ViruSense can be quickly adapt existing Nano Optical Technology to detect LIVE Covid-19 virus via a nose/throat swab in REAL-TIME!

The ViruSense technology will use Covid-19 therapeutic antibodies as part of a solution for a completely new set of coatings to detect the LIVE virus using existing detection technology

The antibody coating will stick to the LIVE Covid-19 virus particles, and the ViruSense sensor will detect the presence of the virus particles “Stuck” to the coating

The time taken to detect the LIVE virus, from putting the sample in the sensor head to result will be less than 30 seconds

The existing sensor technology can already detect much smaller particle sizes than viruses. It is detecting Semi-Volatile Organic Compounds, SVOCs

ViruSense is collaborating with The Rosalind Franklin Institute, Oxford for the following:

- Access to Level 2 Biosafety labs and facilities to perform the adaptation research & development

- Use of the Franklin Institute’s Cvid-19 therapeutic antibodies for use in the adaptation

- Potential access to Level 3 Biosafety laboratories and the Covid-19 virus as and when appropriate.

Virus particles are 100 times > SVOCs, so sensitivity required to detect presence of virus particles already developed

The therapeutic antibodies being used in coating ONLY stick to the COVID-19

The protein “adhesive” to fix antibodies to glass are available

Access to Biosafety laboratories confirmed.

Adaptation Programme and Schedule

Phase 1:

Feasibility of VN-ADS technology adaptation.

The adaptation allows rapid screening taking seconds

The main scientific challenges to be solved are; whether the viruses can be efficiently distinguished from other viruses or macromolecules.

Within approx. 3 months a confirmation of the technology can be verified

A prototype instrument could be achieved within 6 months

Phase 2:

Assuming validation with Pseudovirus, a production-ready design could be ready within 10-12 months assuming sufficient resources to allow parallel working to accelerate testing/validation/results where possible.

The 'Nano Optical Virus Sensor Ltd' Investment Memorandum is available upon request and shares are available on a 'First come - First served' basis.

HMRC ADVANCED ASSURANCE HAS BEEN GRANTED FOR THIS PROJECT

Not all Governments are stating their intentions to ban the sale of Internal Combustion Engines, ICEs. The ones that do seem unconcerned about the challenges in making such claims. Even so, the automotive industry has been left with little choice but to leave no stone unturned in its pursuit of solutions to reduce emissions, including cheating!

And even-though hybrids and electrically-boosted turbos have entered European and US markets as transition technologies, and the overall strategy is to go electric, there are still many markets where the VN KERB solution can be sold/licensed and make money.

In parallel there is a more urgent market opportunity, that of heavy commercial goods, agricultural vehicles and gensets using diesel. Here the reality is a little different. Whilst Governments may state various goals in electrifying HGVs etc. and banning sales there are no alternatives today.

In fact, the Road Haulage Association, representing most of the HGV operators in the UK has stated that recommendations for further reducing road freight emissions are ‘not credible given there are no viable alternatives on the market.’ Since 98% of goods consumed in the UK are transported by HGVs, and the numbers for the rest of the developed world are not dissimilar, the medium-term future for diesel HGVs and agricultural vehicles is secure.

Furthermore, turbo-charging remains the industry solution and anything reducing complexity, size/weight, number of turbos, and increases efficiency and/or reduces emissions is being rapidly adopted.

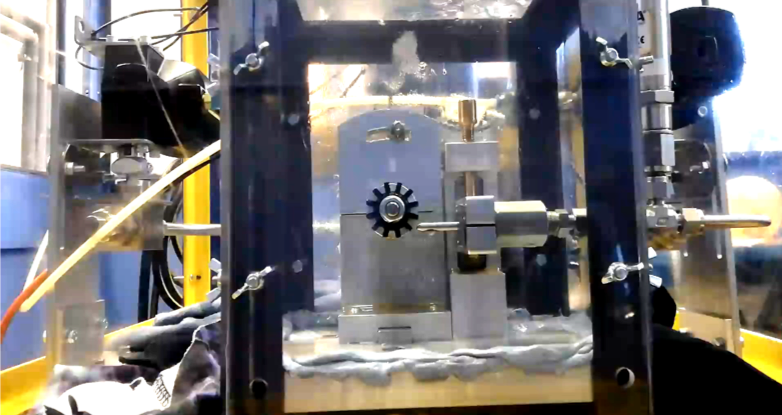

VN KERB now has a technology that delivers this new type of turbo, delivering reduced complexity/weight, improved efficiency and no turbo-lag. A new prototype is being built, ready-for testing on a diesel engine, prior to engagement/demonstration with interested truck/engine manufacturers to deliver a commercial outcome.

There is only £30K of HMRC Advanced Assured SEIS investment remaining before the company is revalued, once engine testing has commenced in the next few months. Don’t delay on your opportunity to make significant gains on your investment by investing now, before an industry opportunist registers commercial interest, as the next stage involves collaboration with an industry partner, and the potential for an Investor exit.

VN KERB is perfectly positioned to benefit from the drive to greater efficiencies, and lack of technological innovation in this space. The team have managed to reduce the overall budget of the programme to deliver TRL 5 by over £300K and are poised to demonstrate the solution on a diesel engine imminently. This next stage will transform the company, and its value.

The Covid 19 pandemic has ravaged the Airline industry, dramatically reducing ticket and new aircraft sales. To compound the pain, the number of litigation claims against them for Aerotoxic Syndrome has increased even further, and to add to its woes the Specialist Class Action legal firms on both sides of the Atlantic are circling. These are the same teams that took on ‘Big Tobacco’ in the 90’s resulting in the Tobacco Master Settlement Agreement

Following a collective case management hearing before Judge Barbara Fontaine, regarding ‘Aerotoxicity Claims’ in 2018, it was agreed to transfer a ‘significant’ number of litigated industrial disease cases to the Royal Courts of Justice (RCJ) in London, ‘achieving greater certainty of outcome and an overall reduction in costs’. It also allows the RCJ to manage cases that have not yet been issued or served (‘intimated’ and ‘future’ claims).

See https://www.classactionlawsuithelp.com/aerotoxic-syndrome-class-action-lawsuit/ - https://www.bc-legal.co.uk/bcdn/925-279-sealed-collective-case-management-order-for-aerotoxic-syndrome-group-litigation.html

This decision has seen a proliferation of individual claims brought by employees or ex-employees of Airlines globally, and the now ‘Open Door Policy’ for claims via the Class Action Specialists.

The result for VN Aerotoxic Detection Solutions is an increasing market opportunity, with the need for ‘real-time’ onboard portable detection of TCP (tricresyl phosphate), and TBP (tributyl phosphate) becoming a necessity for aircraft operators and manufacturers in the face of legislation, which will inevitably follow the successful prosecution of employee claims.

To maximise the opportunity the Directors will seek VC funding both in Europe and the US to accelerate sensor testing, certification, design, manufacturing and distribution.

The low valuation of VN-ADS, the advanced stage of sensor development and the enormous market opportunity make the company an extremely attractive target, and the Directors believe this will provide the opportunity for you, the VN-ADS SEIS and EIS investors to exit with multiple returns on your investment.

There is still £145K of HMRC Advanced Assured EIS equity available at the £20 per share price, and current valuation. Don’t delay, as now is the ideal time for you to invest/reinvest, prior to a potentially significant investment from a VC, delivering you, our SEIS and EIS Investors the multiple return on your investment. Shares will issued be on a first come – first served basis with no maximums per individual.

Members of